Strategies

5 Practical ways to keep your finances safer online

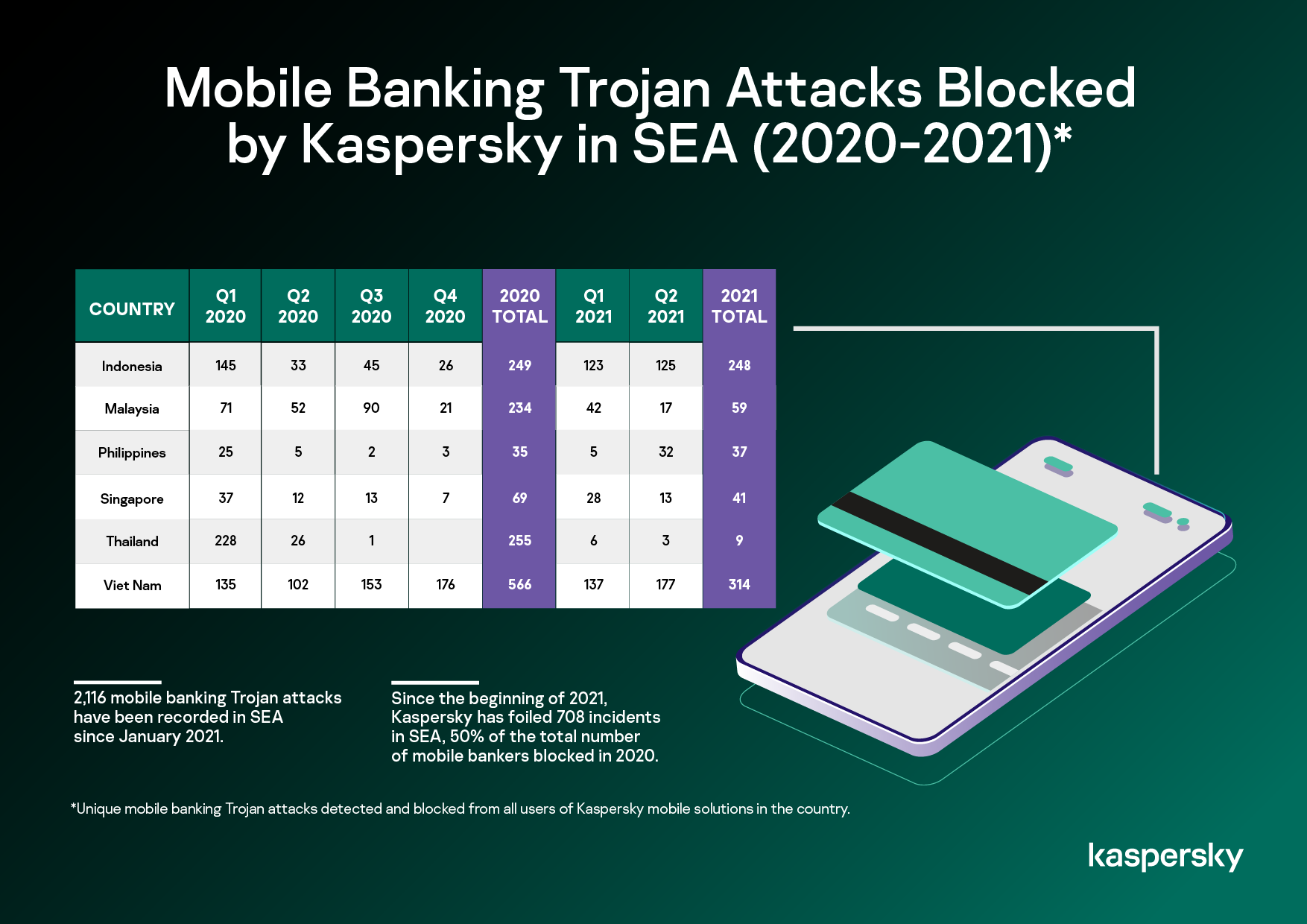

Kaspersky’s fresh data for Q2 2021 showed a 60% increase in mobile banking Trojan attacks blocked in the region versus same period last year.

Kaspersky reveals its Q2 2021 mobile threat report for Southeast Asia (SEA) where it has monitored a 60% uptick in the number of attacks using malicious mobile bankers detected and blocked in the region.

Mobile banking Trojans – or bankers – are used by cybercriminals to steal funds directly from mobile bank accounts. These malicious programs typically look like legitimate financial apps, but when a victim enters their security credentials to try to access their bank account, the attackers gain access to that private information.

Overall, since the beginning of 2021, Kaspersky products have foiled 708 incidents across six countries in SEA. This is already 50% of the total number of mobile bankers blocked in 2020 which was 1,408.

Indonesia and Vietnam logged the most number of incidents during the first half of the year. However, globally, the two countries are not among the top 10 countries affected by this threat. Vietnam is only 27th and Indonesia is 31st as of June this year.

The five countries with the most number of mobile banking Trojan detections in Q2 2021 are Russia, Japan, Turkey, Germany, and France.

*Mobile banking Trojans attacks detected from users of Kaspersky mobile security solutions in the country

While the number of mobile banking Trojan attacks in SEA remains low, 367 incidents from April to June 2021 versus 230 detections during the same period last year, the continuing pandemic continues to force users to start using mobile payment systems.

“We are almost at the second year of the pandemic which has fast tracked the mobile payment adoption in the region at a breakneck speed. During the beginning of this health crisis, our survey already showed that the majority of internet users here have shifted finance-related activities online, like shopping (64%) and banking (47%),” comments Yeo Siang Tiong, General Manager for Southeast Asia at Kaspersky.

The same survey revealed that seven in 10 (69%) are worried about conducting financial transactions online and 42% of the respondents admitted to being afraid about someone accessing their financial details through their devices.

In addition, another Kaspersky report titled “Making Sense of Our Place in the Digital Reputation Economy” discovered that the majority (76%) of 861 respondents from SEA confirmed their intent to keep their money-related data away from the internet. The sentiment is highest among Baby Boomers (85%), followed by Gen X (81%), and Millennials (75%).

“Clearly, there is an awareness about the threats present when we do banking and payment transactions through our mobile phones. But there is still a gap between knowing and acting on it. So to help users from SEA embrace the power of their smartphone and also keep their finances safe, we suggest some practical tips but also encourage everyone to please look into using security solutions as a safety net in case they accidentally clicked a malicious link or downloaded a rogue mobile banking application,” adds Yeo.

Here are some practical tips from Kaspersky which you can do to beef up your money’s safety online:

1. Get a temporary credit card

Cyber criminals have developed incredibly sophisticated techniques and malware that can sometimes thwart your best efforts for safe online shopping. As another level of security for safe online shopping, you can use a temporary credit card to make online purchases, in lieu of your regular credit card. Ask your credit card company if you can be issued a temporary credit card number.

Just remember to avoid using these types of credit cards for any purchases that require auto-renewal or regular payments.

If a temporary credit card is not possible, an alternative is to use a credit card with a low credit limit.

2. Dedicate a computer to online banking and shopping

If you have more than one computer, it may be wise to dedicate one for online banking and shopping only. By avoiding using the computer for any other Internet browsing, downloading, checking email, social networking, and other online activities, you effectively create a ‘clean’ computer that is totally free of computer viruses and any other infections. For added security for safe online shopping, install Google Chrome, with forced HTTPS. This ensures you are visiting only secure websites.

3. Use a dedicated email address

Create an email address that you will use only for online shopping. This will severely limit the amount of spam messages you receive and significantly reduce the risk of opening potentially malicious emails that are disguised as sales promotions or other notifications.

4. Manage and protect your online passwords

Using strong passwords and using a different password for each online account is one of the most important things you can do for safe online shopping. We know it can be difficult to remember so many different passwords, especially when they are composed of numerous letters, numbers, and special characters. But you can use a password manager to aid you in keeping strong passwords for multiple accounts.

5. Use a VPN

If you absolutely must shop online while using public Wi-Fi, first install a VPN (virtual private network). A VPN will encrypt all data that is transferred between your computer or mobile device and the VPN server, preventing hackers from hijacking and viewing any sensitive data you input.

In the Philippines, Kaspersky endpoint solutions like Kaspersky Total Security (KTS) that have a password manager and VPN features is currently included in its 9.9 promos in Shopee and Lazada. Filipino customers can enjoy up to 50% discount.

Strategies

Renting out your place? Human connection key to a successful holiday rental

Warmth, friendliness and a sense of belonging, or the “homely” side of the experience, strengthen guest loyalty, making them more likely to return to the same host. However, these feelings alone didn’t necessarily make guests more likely to recommend the property to others.

BizNews

In-aisle store displays might crowd shoppers and reduce overall sales

Retailers might seek strategies to boost product exposure without also increasing crowding – especially for cart shoppers who may experience greater crowding effects – and that excessive use of in-aisle fixtures will likely dampen sales at the aggregate level rather than increasing it.

BizNews

Structure of online reviews shapes their helpfulness

Reviews that grow increasingly positive are most helpful to readers, while those that turn negative are least helpful. For average-rated products, progressively negative trajectories enhance helpfulness, whereas reviews that start negative and grow positive are least effective.

Modern slavery is a business decision – not an accident

Long-serving CEOs may weaken innovation, study finds

Office owners or managers, take note: Increased risk of bullying in open-plan offices

Profit alone is a poor measure of success, study shows companies can look efficient while harming the planet

Reminder to marketing people: Missing information can misinform

Should emojis be used in workplace communications?

If you’re a perfectionist at work, your boss’ expectations may matter more than your own, research finds

Still developing its approaches? Checking out The Beef Deli in Malolos, Bulacan

If you’re a perfectionist at work, your boss’ expectations may matter more than your own, research finds

Should emojis be used in workplace communications?

Profit alone is a poor measure of success, study shows companies can look efficient while harming the planet

Long-serving CEOs may weaken innovation, study finds

Reminder to marketing people: Missing information can misinform

Office owners or managers, take note: Increased risk of bullying in open-plan offices

Modern slavery is a business decision – not an accident

Biz strategy of Quento: Forget discrimination and capture as many as possible

FFTG as a must-visit cafe… and safe space in Quezon City

5 Video marketing tips

How to successfully market your biz as green

What to do before a ransomware attack

Smart advice to find success

-

BizNews3 weeks ago

BizNews3 weeks agoIf you’re a perfectionist at work, your boss’ expectations may matter more than your own, research finds

-

Tech & Innovation3 weeks ago

Tech & Innovation3 weeks agoShould emojis be used in workplace communications?

-

BizNews3 weeks ago

BizNews3 weeks agoProfit alone is a poor measure of success, study shows companies can look efficient while harming the planet

-

BizNews3 weeks ago

BizNews3 weeks agoLong-serving CEOs may weaken innovation, study finds

-

BizNews3 weeks ago

BizNews3 weeks agoReminder to marketing people: Missing information can misinform

-

BizNews3 weeks ago

BizNews3 weeks agoOffice owners or managers, take note: Increased risk of bullying in open-plan offices

-

BizNews2 weeks ago

BizNews2 weeks agoModern slavery is a business decision – not an accident